Published: Feb 28, 2023 - KFF

The COVID pandemic has disrupted longstanding trends in health spending, utilization, and employment, and created challenges for insurers to accurately predict their costs and set premiums. In the early months of 2020, use of health services dropped sharply, as elective procedures were canceled, and many people delayed or went without care due to concerns of contracting COVID. Utilization has since rebounded, but there are indications that non-COVID care remains below pre-pandemic levels.

In this brief, we examine how insurance markets performed in 2021, the most recent year with annual data. We use financial data reported by insurance companies to the National Association of Insurance Commissioners (NAIC) and compiled by Mark Farrah Associates to look at medical loss ratios and gross margins in the Medicare Advantage, Medicaid managed care, individual (non-group), and fully insured group (employer) health insurance markets through the end of each year. A more detailed description of each market is included in the Appendix.

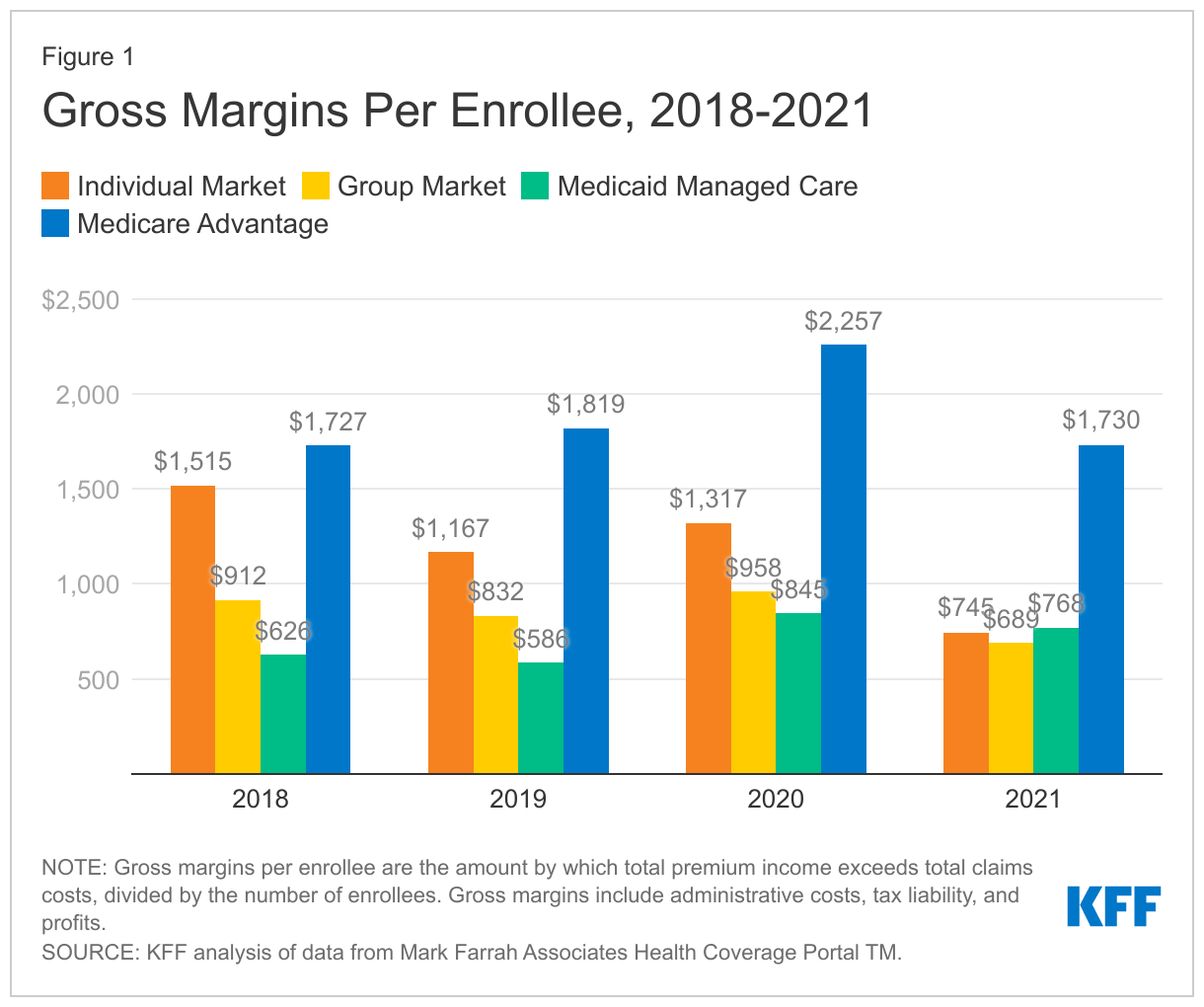

We find that, by the end of 2021, gross margins per enrollee had returned to pre-pandemic levels in the Medicare Advantage market, while gross margins in the individual and group markets were lower than pre-pandemic levels and Medicaid margins were higher than pre-pandemic levels. Medicare Advantage plans have far higher per person gross margins[ore than double those seen in other markets in 2021.

One way to assess insurer financial performance is to examine per enrollee gross margins, or the amount by which total premium income exceeds total claims costs per enrollee per year. Gross margins are an indicator of financial performance, but positive margins do not necessarily translate into profitability since they do not account for administrative expenses or tax liabilities. While gross margins are not equivalent to profitability in absolute terms, changes in gross margins can be indicative of changes in profitability (assuming administrative costs and tax liability are similar).

Through the end of 2021, gross margins in the Medicare Advantage market averaged $1,730 per enrollee, similar to levels seen in 2018 and 2019 before the pandemic began. In 2021, gross margins for Medicare Advantage plans were substantially higher than those seen in the individual ($745 per enrollee), fully insured group ($689 per enrollee), and Medicaid managed care ($768 per enrollee) markets.

Among fully insured group plans, gross margins were 17% lower in 2021 than in 2019. Individual market gross margins were 36% lower in 2021 than in 2019. However, individual market plans were arguably priced too high in the years leading up to the pandemic, as discussed more below. Since the rollout of the ACA Marketplaces in 2014, the individual market has seen substantial volatility in margins (Figure 2) and loss ratios.

On average, gross margins in the Medicaid managed care market were higher in 2021 than they were pre-pandemic. Five publicly traded for-profit firms account for half of all Medicaid managed care organization (MCO) enrollment. Earnings reports from 2021 show continued year-over-year growth in enrollment and Medicaid revenues (for the firms that provide Medicaid-specific revenue information), which could be driving increases in overall Medicaid margins. However, states may use a variety of risk mitigation mechanisms to provide financial protection and limits on financial risk for states and plans that may not be accounted for in the data we used in this analysis. In 2021, more than half of MCO states reported implementing COVID-19 related “risk corridors” (where states and health plans agree to share profit or losses), which led to the recoupment of funds from plans across many states. Gross margins reported for 2021 may not reflect recoupments of funds that may occur after the reporting period.

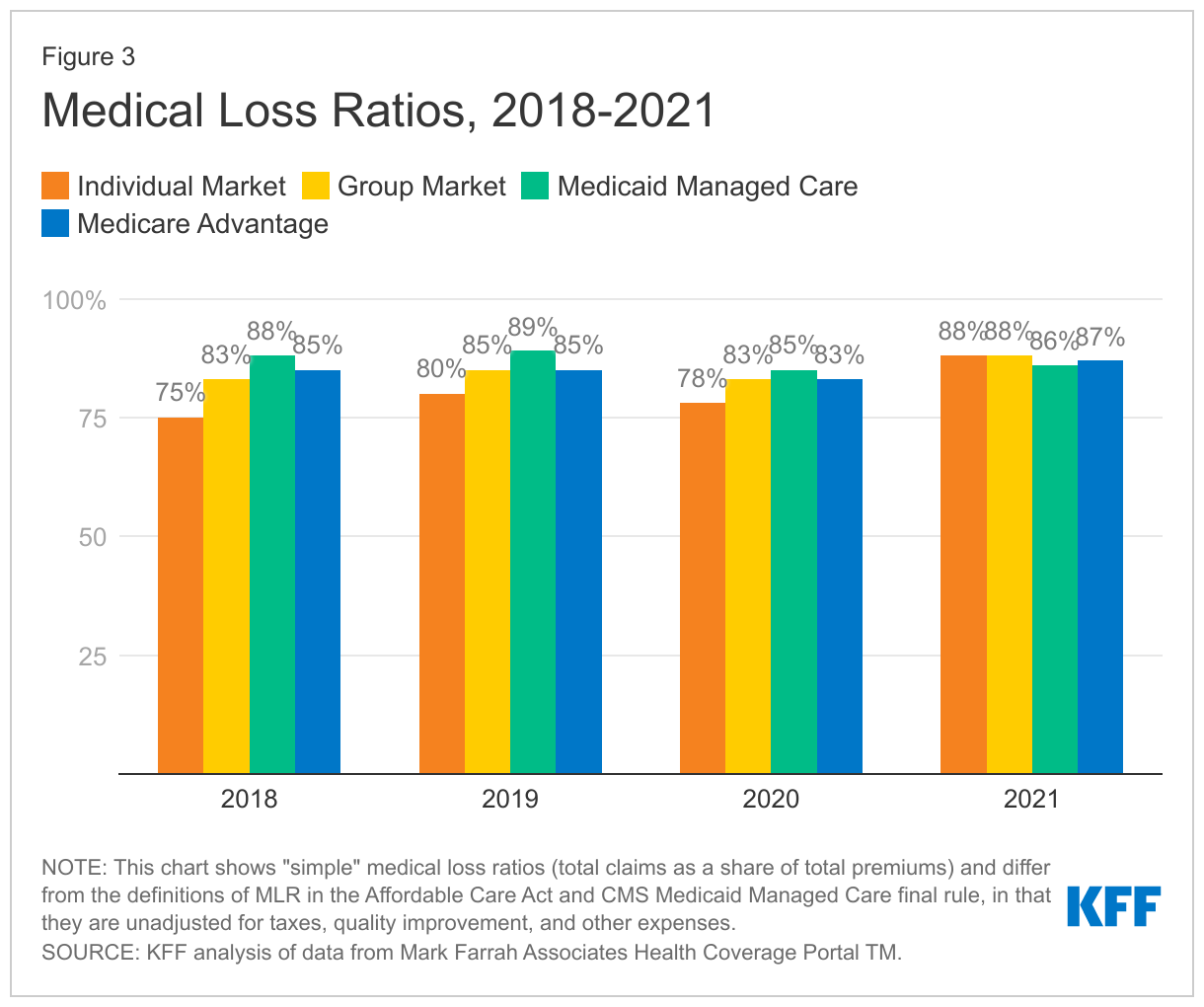

Another way to assess insurer financial performance is to look at medical loss ratios, or the percent of premium income that insurers pay out in the form of medical claims. Generally, lower medical loss ratios mean that insurers have more income remaining after paying medical costs to use for administrative costs or keep as profits. Each health insurance market has different administrative needs and costs, so lower medical loss ratios in one market do not necessarily mean that market is more profitable than another market. However, in a given market, if administrative costs hold mostly constant from one year to the next, a change in medical loss ratios could imply a change in profitability.

Medical loss ratios are used in state and federal insurance regulation in a variety of ways. In the commercial insurance (individual and group) markets, insurers must issue rebates to individuals and businesses if their loss ratios fail to reach minimum standards set by the ACA. Medicare Advantage insurers are required to report loss ratios at the contract level; they are also required to issue rebates to the federal government if their MLRs fall short of required levels and are subject to additional penalties if they fail to meet loss ratio requirements for multiple consecutive years. For Medicaid MCOs, CMS requires states to develop capitation rates for Medicaid to achieve an MLR of at least 85%. There is no federal requirement for Medicaid plans to pay remittances if they fail to meet their MLR threshold, but a majority of states that contract with MCOs do require remittances in at least some cases.

The medical loss ratios shown in this issue brief differ from the definition of MLR in the ACA and CMS Medicaid managed care final rule, which makes some adjustments for quality improvement and taxes, and do not account for reinsurance, risk corridors, or risk adjustment payments. (Notably, the health insurer tax, which has been permanently repealed starting in 2021, was in effect in 2018 and 2020, but not 2019 or 2021). The chart below shows simple medical loss ratios, or the share of premium income that insurers pay out for benefits, without any modifications (Figure 3).

In 2021, loss ratios were similar across all markets. Simple loss ratios were 87% in the Medicare Advantage market, 88% in both the individual and fully insured group markets, and 86% in the Medicaid managed care market. However, because each market has different administrative needs and costs, this does not imply that the markets are similar to each other in profitability.

Rather, we can look at changes in the direction of loss ratios as an indication of changes in profitability in a given market. Relative to 2019, average loss ratios in the Medicaid managed care market remain lower (implying increased profitability), while average loss ratios in the group and Medicare Advantage markets were somewhat higher than pre-pandemic levels.

Individual market loss ratios in 2021 are substantially higher than those seen in the years leading up to the pandemic. As mentioned earlier, 2018 and 2019 were exceptionally lucrative years for the individual market. Many plans fell short of the ACA’s medical loss ratio requirements and were therefore required to issue large rebates to consumers based on their 2018 and 2019 experience.

Using annual financial data reported by insurance companies to state regulators, it appears health insurers in the Medicare Advantage market saw similar financial performance in 2021 as they did in the years leading up to the pandemic. Insurers in the Medicaid managed care market, meanwhile, saw somewhat better performance and commercial insurers (particularly in the individual market) saw worse performance than in the years leading up to the pandemic.

Across all markets, 2021 gross margins were by far the highest for Medicare Advantage plans. Medicare Advantage plans have both higher average costs and higher premiums (largely paid by the federal government), because Medicare covers an older, sicker population. So, while Medicare Advantage insurers spend a similar share of their premiums on benefits as other insurers in other markets, the gross margins『hich include profits and administrative costs{f Medicare Advantage plans tend to be higher.

Potentially spurred by the prospect of strong financial returns, the Medicare Advantage market has grown substantially in the last decade, with more than 50% of eligible beneficiaries expected to enroll in a Medicare Advantage plan in 2023. Insurers that fall short of required loss ratio requirements for multiple years face penalties, including the possibility of being terminated. To avoid such a risk, some Medicare Advantage insurers with loss ratios below 85% may take this opportunity to offer new or more generous extra benefits, such as over-the-counter allowances, meals following hospital stays, or transportation, in addition to gym memberships, dental, vision and hearing benefits that are offered nearly universally to help retain and attract new enrollees.

Looking ahead to coming years, the pandemic’s effect on insurer financial performance remains uncertain. The direct costs associated with the pandemic remain hard to predict, as treatment costs may rise or fall depending on new variants or increased population immunity. Additionally, the commercialization of COVID-19 vaccines and treatments will lead to higher prices per dose, but total costs will also depend on the number of doses (e.g., uptake of boosters), which is difficult to predict. There are also the indirect effects of the pandemic to consider. Health care utilization has mostly rebounded to pre-pandemic levels, though there are indications utilization remains suppressed for non-COVID care and there could be additional pent-up demand for care that had been missed or delayed. For Medicaid, the unwinding of the continuous enrollment provision on March 31 means states will begin disenrollments that have been paused since the start of the pandemic and could result in millions of individuals losing Medicaid coverage. Medicaid MCOs may see the overall acuity of their membership increase, which could have implications for overall utilization and costs looking ahead.